Debt Recycling: The "Secret" Strategy for Building Tax-Effective Wealth

Most homeowners view their mortgage as a burden to be cleared as quickly as possible. However, savvy investors often use a strategy called Debt Recycling to make their debt work harder. By converting "bad" debt into "good" debt, you can build an investment portfolio while simultaneously paying off your home.

Understanding the Fundamentals

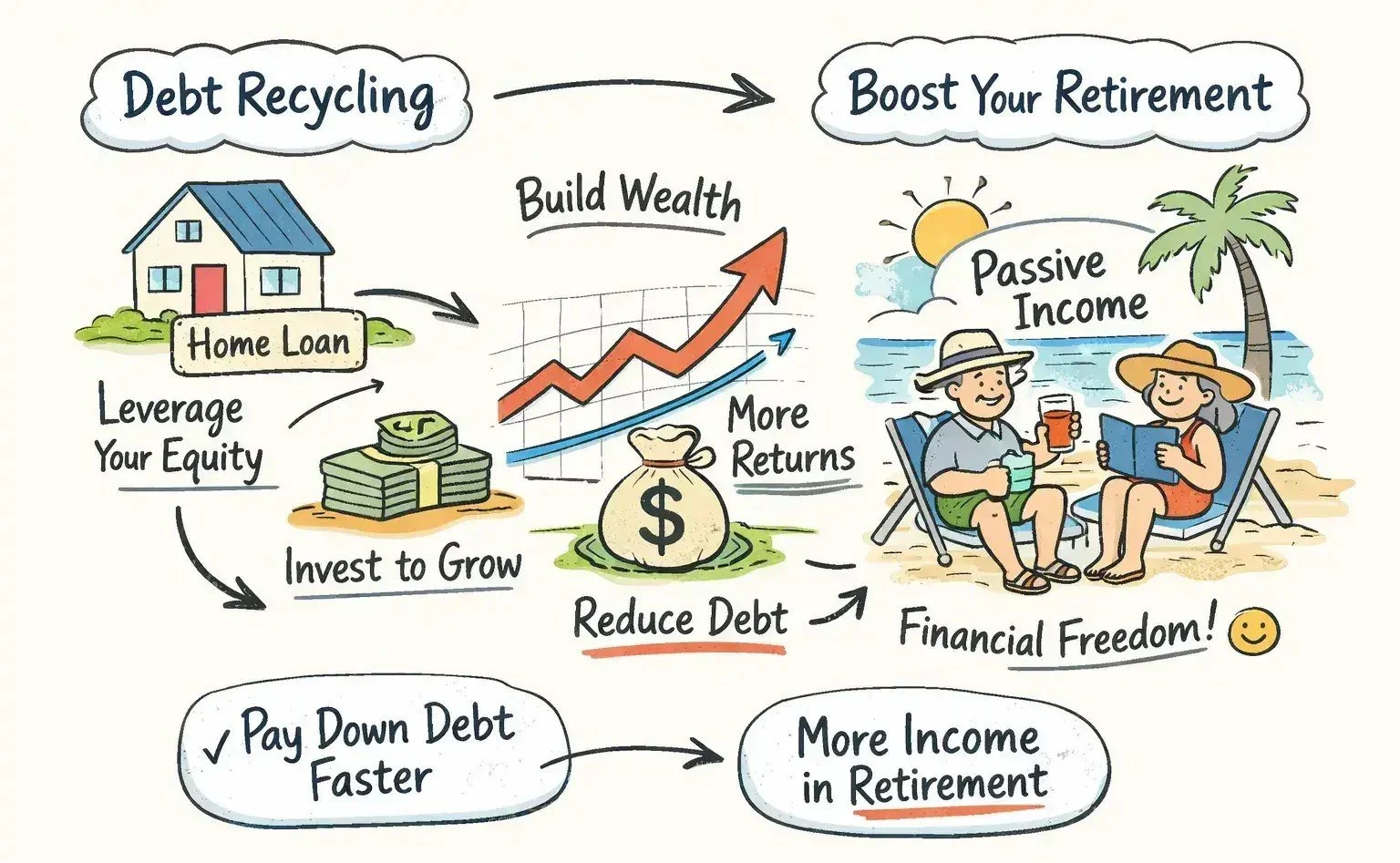

At its core, debt recycling involves taking the equity in your home and using it to fund income-producing assets. The goal is to replace a non-deductible loan (your home mortgage) with a tax-deductible loan (an investment loan).

Non-deductible Debt: Interest paid on your primary place of residence is generally not tax-deductible.

Deductible Debt: Interest paid on funds borrowed to purchase income-producing assets (like shares or investment property) can often be claimed as a tax deduction.

How the Strategy Works

The process is cyclical and requires a disciplined approach to cash flow management. Here is the typical workflow:

Step 1: Use surplus cash or savings to pay down a portion of your non-deductible home loan.

Step 2: Redraw that same amount from a separate investment loan sub-account.

Step 3: Invest those borrowed funds into income-producing assets, such as diversified ETFs or investment properties.

Step 4: Use the income generated from these investments (and any tax refunds) to further pay down the original home loan.

The Power of Compounding and Tax Deductions

The "magic" happens because you aren't actually increasing your total debt; you are simply changing its "color" from non-deductible to deductible. Over time, the tax savings and investment growth can significantly accelerate your path to financial independence. According to the Australian Taxation Office (ATO), for interest to be deductible, the borrowed funds must be used for the purpose of gaining or producing assessable income.

Key Risks to Consider

While the benefits are clear, debt recycling is not without risk. It is a form of gearing (borrowing to invest), which magnifies both gains and losses.

Market Volatility: If your investments decrease in value, you still owe the full loan amount.

Interest Rate Hikes: Rising rates can increase the cost of servicing the debt.

Tax Compliance: You must keep your investment and personal loan accounts strictly separate to satisfy ATO requirements.

Frequently Asked Questions (FAQ)

1. Does debt recycling increase my total debt? No, the primary goal of debt recycling is to maintain the same level of debt but change its purpose. You pay down the non-deductible portion and immediately redraw it for investment, keeping the total balance neutral.

2. What can I invest in for the interest to be tax-deductible? Under ATO guidelines, you must invest in assets that have a reasonable expectation of producing assessable income, such as dividend-paying shares, managed funds, or residential investment properties.

3. Do I need a specific type of bank account? Yes. It is crucial to use a "split loan" or a separate investment sub-account. Mixing personal and investment funds in a single account can make it impossible to track deductible interest, which the ATO may challenge.

4. What happens if my investment doesn't pay a dividend? If an investment is purely for capital growth and has no prospect of producing income (like certain "growth" stocks or crypto-assets), the interest on the loan may not be tax-deductible. Always check the income-producing intent of the asset.

5. Can I use this strategy with a small amount of equity? While possible, it is most effective when you have a significant "buffer" of equity. Most lenders require you to maintain a Loan-to-Value Ratio (LVR) of 80% or less to avoid Lenders Mortgage Insurance (LMI).

Is It Right for You?

This strategy is most effective for individuals with a steady income, a long-term investment horizon, and a comfortable level of equity in their homes. It requires a precise loan structure, often involving split loans or offset accounts, to ensure the interest remains clearly deductible.

Connect with our Linkins team today for expert support in structuring your finances and exploring if debt recycling aligns with your long-term wealth goals.

--

Disclaimer:

The information and content provided in this publication are purely for informative purposes. It is not meant to serve as advice, and you should not act specifically on the basis of this information.